We recommend appointing a law firm with experience of early stage equity fundraising to handle the legal documentation for the round. It is common for early stage companies to have articles of association and shareholders agreements that don’t function properly – and this often only emerges when these documents are put to the test, for example, through conflict with a shareholder or a shareholder employee leaving the business.

Law firms are typically appointed once a term sheet has been issued to investors and there is a reasonably high likelihood of agreement along the lines of the terms proposed. As a term sheet is not legally binding, it is not essential to have legal input up until this stage, but you may wish to seek a friendly view of your proposed term sheet in advance of circulation.

A clear matter scope and fee arrangement is important to avoid unexpected costs. We recommend working to fixed price scopes and agreeing to variations where there is scope creep. Fee estimates should be treated with some caution as they are not a cap.

Some essential items for the matter scope:

Some additional items you may require:

We recommend appointing a law firm with experience of venture stage equity fundraising (Series A, B etc.) to handle the legal documentation for the round.

Law firms are typically appointed once a term sheet has been issued and there is a reasonably high likelihood of agreement along the lines of the terms proposed. As a term sheet is not legally binding, it is not essential to have legal input up until this stage, but you may wish to in the course of negotiating the term sheet, in part to avoid more protracted negotiation during finalisation of the legal documentation.

A clear matter scope and fee arrangement is important to avoid unexpected costs. We recommend working to a fixed price scope and agreeing to specific variations where there is scope creep. Fee estimates should be treated with some caution as they are not a cap.

It is usual for institutional investors to provide the first draft of the legal documentation suite, in particular, the revised articles of association and shareholders agreement. This is because most have a standard set of documents that are applied across their portfolio. There are significant similarities in the structure of these documents across the industry which makes it easier for funds to co-invest. The British Venture Capital and Private Equity Association (BVCA) provide standard documents that are frequently used as a starting point.

As a result, your legal counsel’s primary role will be in reviewing and preparing commentary and amendments to the documentation.

Some essential items for the legal scope:

Some additional items you may require:

If the fundraise will be under the EIS or VCT tax schemes:

If the investor will undertake legal due diligence:

A term sheet sets out the principal terms that will form the basis of the final transaction documentation, in particular, the articles of association and the shareholders agreement, that will be entered into on completion of the transaction. The term sheet is not intended to be legally binding (with the exception of the confidentiality clause) and serves to act as a guide.

Before issuing a term sheet, you will need to have decided upon the principal terms surrounding the proposed seed round, though these can change through the course of negotiations up to completion.

In previous sections we have covered valuation (pre and post money valuation and the subscription price), and cap tables, where you calculate the percentage equity that new investors will hold.

There are a number of other terms that govern the interaction between the Company, the Board and the shareholders, and the commercial terms of the new investment.

We have prepared a template term sheet that contains a number of key terms and can be tailored to fit your specific seed round.

Note that institutional funds will ordinarily issue their own term sheet for you to review and agree. For seed rounds comprising individuals and smaller seed funds, you will be expected to provide a term sheet.

Size of the Round

The total amount of money (New Equity) being raised as part of the Seed Round, for example £500,000.

Post Money Equity Valuation

The valuation at which the funding will be raised, calculated by:

It is not necessary to also include the Pre Money Equity Valuation, but if requested it is:

Subscription Price

The price per share paid by the Seed Investors, calculated by:

Which should also equal:

Subscription Shares

The total number of shares that Seed Investors will subscribe for:

Proportion of Total Equity held by Seed Investors

This is the equity stake that the Seed Investors will hold in the business post the fundraise:

Ranking of Shares

This term sets out how the newly issued shares will rank relative to the existing shares in issuance. Is it typical for seed rounds for ordinary shares to be issued, i.e. just more of the same class as currently in issuance and held by the founders. In this instance, the newly issued shares will rank equally and participate equally with existing shares on voting rights, dividends and on a return of capital.

A new class of share could be created if they were to hold preferential or different legal or commercial rights and is significantly more likely to be required if raising from a seed fund or other institutional investor.

Note that one of the eligibility criteria for a round to be SEIS or EIS eligible is that newly issued shares are full-risk ordinary shares that are not redeemable or carry any preferential rights to the company’s assets on a winding up.

Information Rights

It is common to provide some information to your investors on a monthly, quarterly or annual basis. This may depend on how involved your investors wish to be, and may be as limited as the Company’s annual accounts, or may also include:

Investor Director

If you intend to offer investors the right to appoint a Non Executive Director, then you will need to include this clause. It is not necessarily a pre-requisite or expected and depends on your investors. They may seek the right to appoint one Non Executive Director between them, usually voted for in proportion to their shareholdings.

Warranties

Include this term if the Directors, Founders and/or the Company will provide warranties to the seed investors. Warranties may be limited to the accuracy of the current share capital, or may be more thorough and include the reasonableness of assumptions underpinning the business plan, the status of the Company’s trading, any outstanding liabilities or litigation etc. They are often minimal or excluded from seed rounds.

Option Scheme

If you intend to put in place an option scheme, for example an EMI scheme, as part of the transaction or shortly thereafter, then include a clause in reference to this, setting out the maximum equity percentage of the company the option scheme will represent.

New Issue of Shares

This clause summarises the ability of the company to issue new shares, and usually permits the company to issue shares as part of any specific option scheme, or with the consent of a proportion of the shareholders. Otherwise issuances may be offered pro-rata to existing shareholders.

Transfer of Shares

These set out the rights of each shareholder to transfer their shares to another individual or entity. It is common to have in place permitted transfers, which allow shareholders to transfer all or a portion of their shareholdings to immediate family or family trusts. Otherwise, it may be drafted that any shares intended to be transferred are to be offered first to the existing shareholders pro-rata to their shareholding.

Drag Along

A drag along right entitles a certain proportion of the shareholders (usually the majority) to force smaller shareholders into a sale of the company to a third party purchaser. This can be necessary to prevent smaller shareholders from refusing to sell their shares and preventing an exit event.

Tag Along

A tag along right entitles a shareholder to participate if an offer is made for a majority of the issued shares, on the same terms as those offered to the majority shareholder(s).

Investor Consents

Investor consents are sometimes requested by a group of new investors to give them some protection and control over key decisions made by the directors, the company and/or the majority shareholders.

Investor consents usually require a certain proportion of shareholders consent to a particular list of actions. Where this percentage is set depends on your current shareholder structure. If, say, following the seed round two co-founders will hold 80% of the shares and the new investors will hold 20%, then there is no point in setting the threshold at 75% as this affords no protection to the new investors – the co-founders could vote together and ignore their consent. In this instance, the threshold may be set at 85% so that if both co-founders agree, they will still require a further 5% to proceed.

The list of consents usually comprises significant decisions, such as a winding up or sale of the company, issuance of new equity, significant capital expenditure or the disposal of assets.

Pre-emption

Pre-emption rights allow shareholders to participate in future share issuances or fundraises if they wish to, and thus reduce or prevent their equity shareholding from being diluted.

Leaver provisions

Leaver provisions set out what happens to the shares held by directors that leave the company. They will usually define a “good leaver” and a “bad leaver”, for example, a bad leaver may be someone who is dismissed or who resigns. All of, or a portion of, their shares may be subject to repurchase by the company and any remaining shares are likely to lose their voting rights (be “disenfranchised”).

The purpose of leaver provisions is to discourage individuals from leaving, to ensure that those individuals that are no longer involved in the company are not able to vote on key decisions and that equity is returned to the company to incentivise a replacement, if necessary.

It is not essential to set these out in a term sheet for a seed round; however, investors may ask for your intentions with regards to these clauses.

Following a successful presentation and early due diligence, an offer from a venture investor will come in the form of a term sheet (sometimes called a “heads of terms”).

A term sheet sets out the principal terms that will form the basis of the final transaction documentation, in particular, the articles of association and the shareholders agreement, that will be entered into on completion of the transaction. The term sheet is not intended to be legally binding (with the exception of the confidentiality clause) and serves to act as a guide.

While specific terms can be negotiated at the point of drafting the final investment documentation, the purpose of the term sheet is to ascertain alignment on the deal proposed, so this is the time to raise and discuss any proposed amendments.

In this section we summarise the terms you may come across in a venture term sheet, and what they mean.

Valuation

This will usually be presented as a certain amount invested for a certain equity percentage. From this, you can calculate the valuation that the investor has applied to the business (the post money equity value, pre money equity value and enterprise value).

For example, an investment of £2,000,000 for newly issued shares representing 25% of the business.

The value of the business is then:

Arrangement fee

Some funds charge an arrangement fee that becomes due when the deal completes and is usually based on a percentage of total funds raised. Fees vary significantly between funds – they are relatively uncommon among venture capital firms but more typical of later stage funds, such as growth capital or private equity funds. The transaction fee usually serves the purpose of covering the cost of the process for your investor and is also one of theirs sources of income. Some investors also charge an ongoing monitoring fee.

Ranking of Shares

The term sheet will set out how the newly issued shares will rank relative to the existing shares in issuance.

Institutional investors and funds will almost always seek a new class of share to be issued alongside the existing ordinary shares held by the founders and early seed investors.

This is so that specific rights can be attached to this new class of share – these rights may be economic and/or legal in scope.

Note that one of the eligibility criteria for a round to be EIS eligible is that newly issued shares are full-risk ordinary shares that are not redeemable or carry any preferential rights to the company’s assets on a winding up. This may impact the extent of rights attached to the new class of share.

Priority return or liquidation preference

Investors may ask that their investment is returned to them before the remaining proceeds are split pro-rata between the ordinary shareholders. A multiplier may be applied to this right, for example, a 2x liquidation preference means that the investor is entitled to twice their investment before remaining proceeds are divided up. The exit valuation at which this will apply may vary – it may only be relevant if you sell your business below a certain value, and hence is there to provide the investor with protection if things don't go to plan.

Liquidation preferences of 1.0x are relatively common. Up to 2.0x are occasional and above 2.0x are relatively rare.

The commercial terms of a deal need to be considered as a whole and not viewed in isolation, so consider this alongside the implied valuation, dilution and any other economic terms within the term sheet.

Some companies agree to higher liquidation preferences in return for giving away a lower equity stake in the business.

Participation

Investors that hold preferred shares may also ask for a portion of the proceeds owed to ordinary shareholders in the event of a sale, called “participating preferred shares”. There may be a cap applied to this participation, for example, the investor may receive a portion of the proceeds until they have received 2x their initial investment, and after that all proceeds will be divided among the remaining ordinary shareholders and the investor will not participate any further.

Dividend policy

Investors may request the right to participate in any dividends distributed to ordinary shareholders. In certain circumstances, they may also seek some form of preferred dividend, paid before any dividends to ordinary shareholders, provided that the company has sufficient reserves. They may also have the ability to veto any dividend policy.

Drag Along

A drag along right entitles a certain proportion of the shareholders (usually the majority) to force smaller shareholders into a sale of the company to a third party purchaser. This can be necessary to prevent smaller shareholders from refusing to sell their shares and preventing an exit event. Drag along rights are very common in venture term sheets as investors need to be confident of securing an eventual exit.

Tag Along

A tag along right entitles shareholders to participate if an offer is made for a majority of the issued shares, on the same terms as those offered to the majority shareholder(s).

Pay to Play

This clause requires that all investors contribute a certain amount to any future fundraising, and if they don’t they may lose certain rights, for example, be forced to convert their preferred shares into ordinary shares and thus lose their preferred rights. If you are raising money from multiple investors, those investors that are not well placed to provide further funding down the line may be put off by this clause as they may be faced with an inevitable loss of rights.

Information Rights

Investors may require certain information to be made available to them on a monthly, quarterly or annual basis, which could include:

Non Executive Director or Investor Director

Institutional investors may require the right to appoint a Non Executive Director to the Board – this may be an individual from their own firm or an individual they introduce from their network, or both. They may also have the right to make this person the Chairman.

If a number of funds are participating, this right is usually reserved for the lead investor to prevent the board becoming too crowded.

Warranties

The directors, founders and/or the Company will be required to provide warranties to the new investors. Warranties will vary in scope depending on the investor, from warranting the accuracy of the current share capital, to the reasonableness of assumptions underpinning the business plan, the status of the Company’s trading and any outstanding liabilities or litigation.

If you agree the term sheet and progress through due diligence to completion, you will produce a disclosure letter which can be used to disclose any relevant information against these warranties and protect yourself and the company from a claim being made in respect of those specific items. For example, you may be required to warrant that there are no current employment cases against the company – if there were to be one, this would be described in the disclosure letter.

Option Scheme

If you intend to put in place an option scheme, for example an EMI scheme, as part of the transaction or shortly thereafter, then this should be explicitly mentioned in the term sheet and should set out the maximum percentage of the issued share capital that the option scheme will represent.

Investors will take dilution from options into account when calculating their anticipated return. They may seek a higher equity percentage to compensate for a large option pool.

Up to 10% of equity is relatively common for an option pool to be allocated to key members of the team.

Transfer of Shares

These set out the rights of each shareholder to transfer their shares to another individual or entity. It is common to have in place permitted transfers, which allow shareholders to transfer all or a portion of their shareholdings to immediate family or family trusts. Otherwise, it may be drafted that any shares intended to be transferred are to be offered first to the existing shareholders pro-rata to their shareholding.

Investor Consents

Investor consents are often required by minority investors to provide them some protection and control over key decisions made by the directors, the company and/or the majority shareholders.

Investor consents usually require that a certain proportion of shareholders consent to a particular list of actions. Where this percentage is set depends on your current shareholder structure. If, say, following the fundraise two employee shareholders will hold 80% of the shares and the new investors will hold 20%, then there is no point in setting the threshold at 75% as this affords no protection to the new investors – the existing shareholders could vote together and ignore their consent. In this instance, the threshold may be set at 85%, say.

The list of consents usually comprises significant decisions, such as a winding up or sale of the company, issuance of new equity, significant capital expenditure, key hires or the disposal of assets.

Pre-emption

Pre-emption rights allow shareholders to participate in future share issuances or fundraises if they wish to, and thus reduce or prevent their equity shareholding from being diluted.

Leaver provisions

Leaver provisions set out what happens to the shares held by directors or employees that leave the company. They will usually define a “good leaver” and a “bad leaver”, for example, a bad leaver may be someone who is dismissed or who resigns, and a good leaver may be someone who becomes incapacitated through illness or dies. All of, or a portion of, their shares may be subject to repurchase by the company and any remaining shares are likely to lose their voting rights (be “disenfranchised”).

The purpose of leaver provisions is to discourage individuals from leaving, to ensure that those individuals that are no longer involved in the company are not able to vote on key decisions and that equity is returned to the company to incentivise a replacement, if necessary.

Swamping rights

Minority investors may define certain circumstances in which they will have the ability to take voting control, i.e. will hold 51% or more of the voting rights in the company. These rights may be invoked for any reason or could have specified triggers, for example, the company underperforming, a key director leaving the business or a breach of banking covenants.

Assessing how much capital to raise requires an understanding of the company’s forecast financial performance and cash burn rate.

To do this, you will need to prepare a financial forecast model that includes a cash flow. If you don’t already have one, see our dedicated guide to creating a venture-stage financial model.

Ensure that you include in your plan what you intend to invest the money in, for example, marketing expenses, new hires, investment in technology. If your cash does not dip into the negative then you may not need to raise funding at all.

With your assumptions included, the cash flow will illustrate the quantum of cash required, equal to the lowest negative balance.

Add an appropriate quantum of headroom to this figure to calculate the total funding requirement.

While this will vary for each business and your risk appetite, one approach is to assume that the business should be able to survive for 3 months in the instance that all income ceases. This would give you a window of time to establish new income or raise funding.

Understanding your cash burn rate, that is, the rate at which your business depletes cash, is required to estimate this figure. Take your monthly cash burn rate, deduct your monthly income and multiply this by the number of months for which you want to "stay alive", say, three months. Now you have an estimate for what your cash headroom should be.

You may wish to add to this figure if:

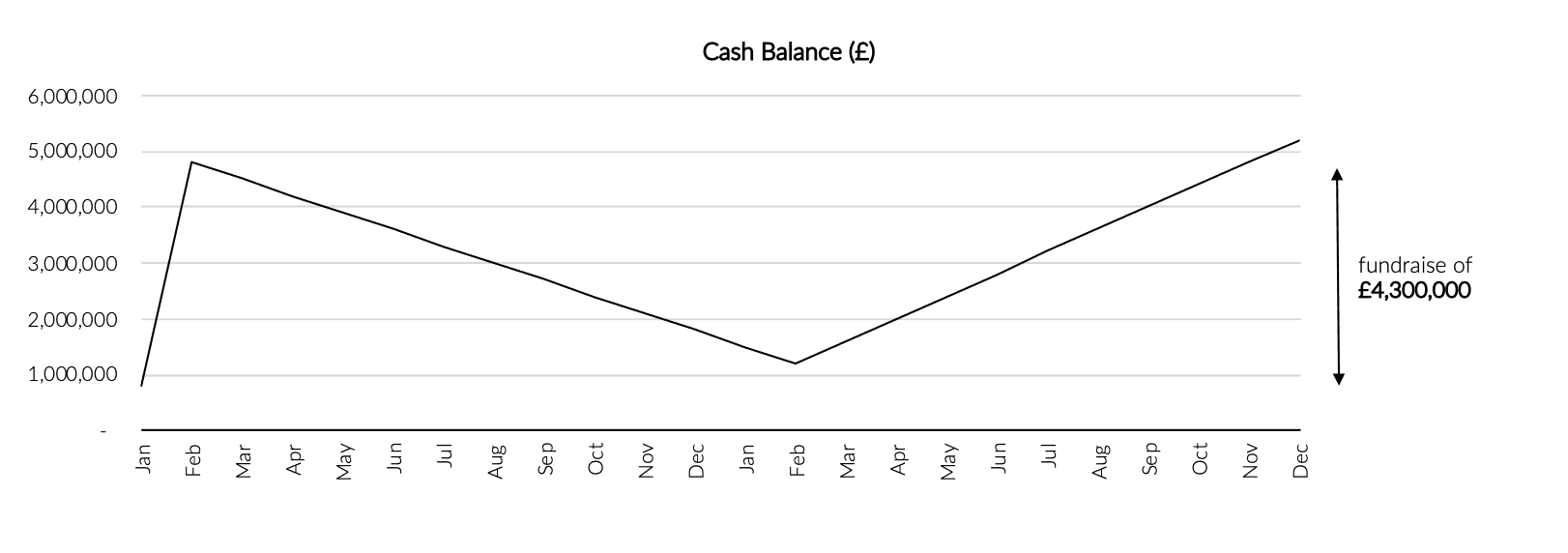

In this example the business is depleting cash because it is investing, and intends to continue investing, heavily in costs and capital expenditure, which exceed income. With turnover growing rapidly, the business is expected to become cash generative in approximately a years’ time.

Funding is required to sustain the business until this point is reached and allow it to continue to invest in growth. The business is expected to run out of cash in April and reach a cash low point of minus £3,100,000 the following February.

With significant investment in marketing and headcount, the cash burn rate is approximately £300,000 per month and monthly turnover is £100,000. An estimate of appropriate cash headroom is therefore:

The total cash requirement is:

Assuming a successful raise in February, the cash flow now looks like this:

In the example above, through turnover growth the business is expected to become profitable in the foreseeable future. The investment of £4,300,000 is sufficient to plug the cash gap until profitability is sufficient to fund future growth – this business may therefore not need further capital.

Many businesses require multiple rounds of financing as profitability will take longer to achieve or a more aggressive investment strategy is envisaged.

In this instance, the cash graph will continue to show cash depletion even with new investment. Investors will seek reassurance that enough cash is being raised. A general rule of thumb is to ensure that the investment will provide sufficient cash headroom for at least two years post investment. This means that you expect to be doing your next round in two years’ time.

The alternative is to raise funding that covers a longer period, for example, five years. Whilst this brings greater certainty of cash headroom, it often comes at a cost. A growing business that undertakes a larger round, to be deployed over 5 years, will typically incur higher dilution than an identical business that raises the same amount in smaller tranches over the period, assuming that the value of the company rises with time. Fundraising is exceptionally resource intensive and time-consuming, though, so there is a balance to be reached between raising enough cash and not too often.

When doing a seed round, investors will usually expect you to come up with a proposed price for the round, at least as a starting point.

It is very difficult to price early stage companies, as it involves a significant amount of judgement and guesswork. The core valuation principles that apply to large, listed companies, stock markets and even private equity backed companies, are difficult to apply as they rely heavily on multiples of profit and do not take into account the rapid growth rate of many small companies.

Ultimately, the theorems underpinning corporate valuation are a representation of the collective view held by investors of an appropriate risk-adjusted return. Therefore, once you have a starting point for discussion with investors, you will soon find out whether they agree that it represents an attractive risk-adjusted return through uptake and / or negotiation. The objective being to settle on a price that all parties are comfortable with.

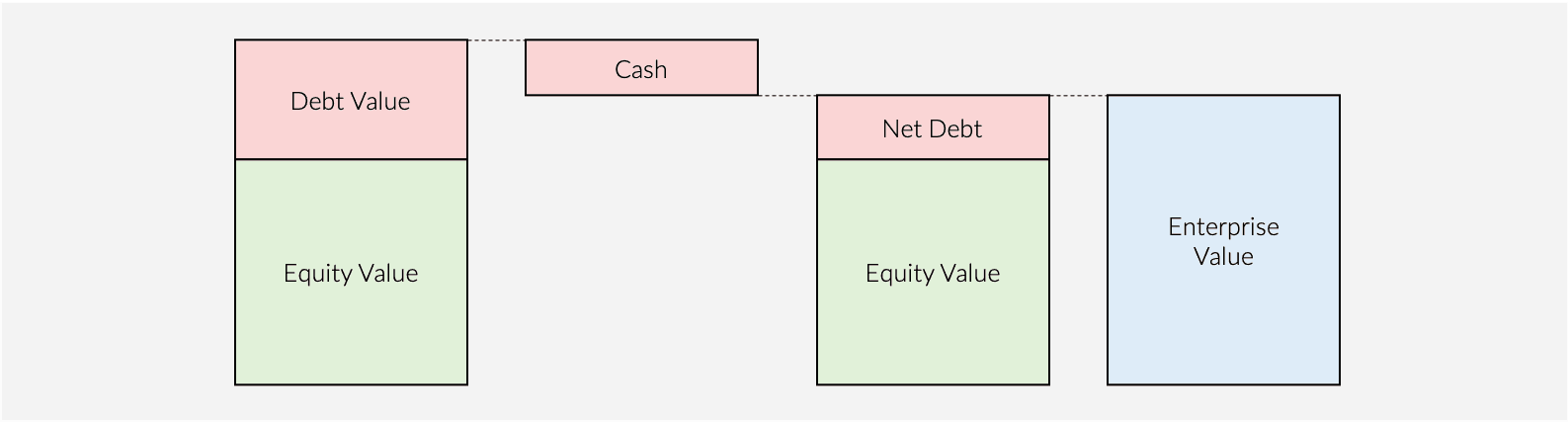

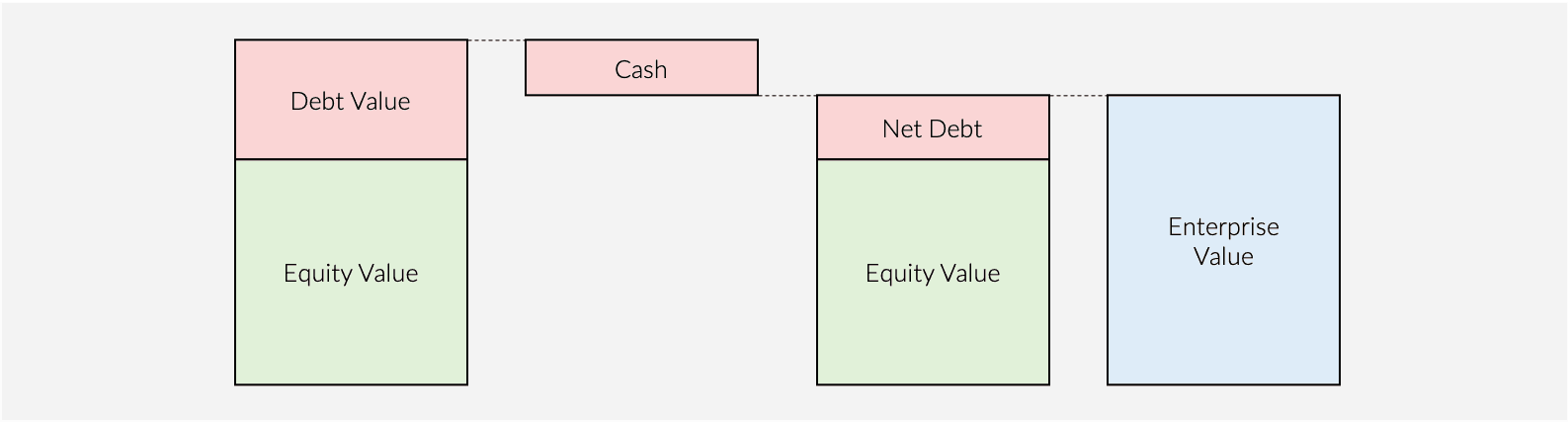

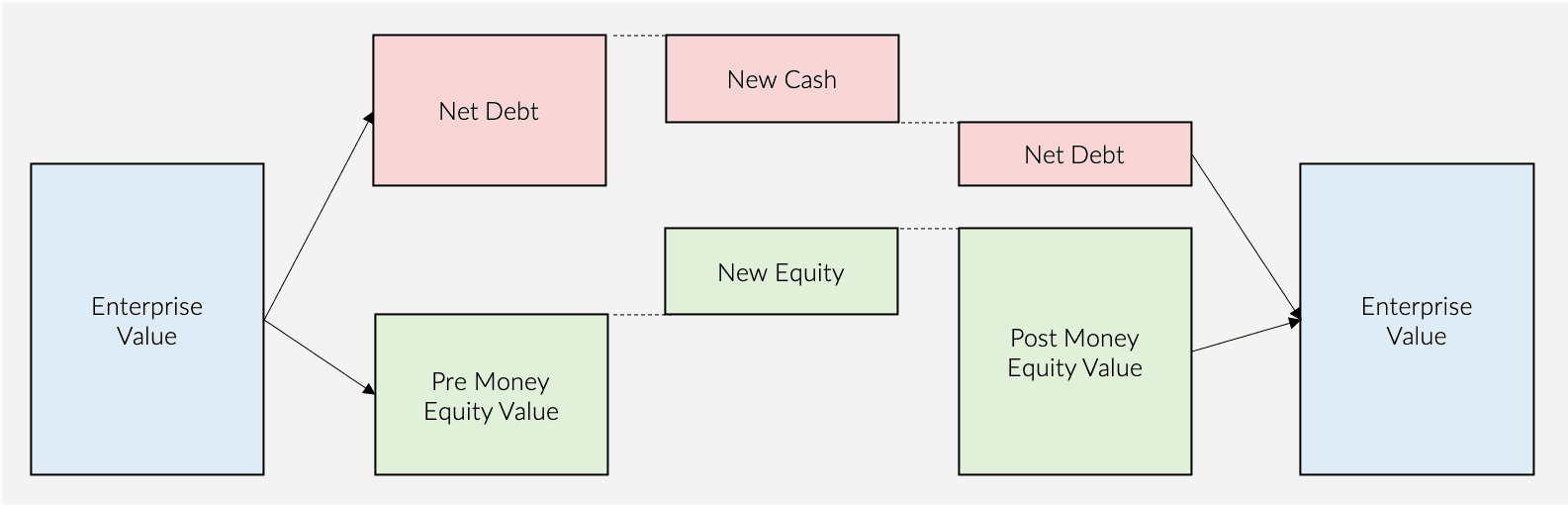

The value of a business is called the “Enterprise Value” or “EV”. It is a common misconception that valuation increases when you raise equity – this is incorrect. It is not possible to alter the value of a company through changing the way in which it is financed – only through utilising that investment to generate more money, can value be created.

The EV of a business therefore remains the same before and after raising money. The terms pre-money equity value and post-money equity value refer to a portion of the EV only.

The EV represents the total value of claims that each stakeholder has on the business. Stakeholders comprise:

Debtholders rank in priority to shareholders.

EV is essentially the value owned by the debtholders (“Debt Value”) plus the value owned by the shareholders (“Equity Value”), minus the cash sitting on the balance sheet. If there is cash on the balance sheet, then this can theoretically be used to pay back some of the debtholders. Debt minus cash is referred to as Net Debt and therefore:

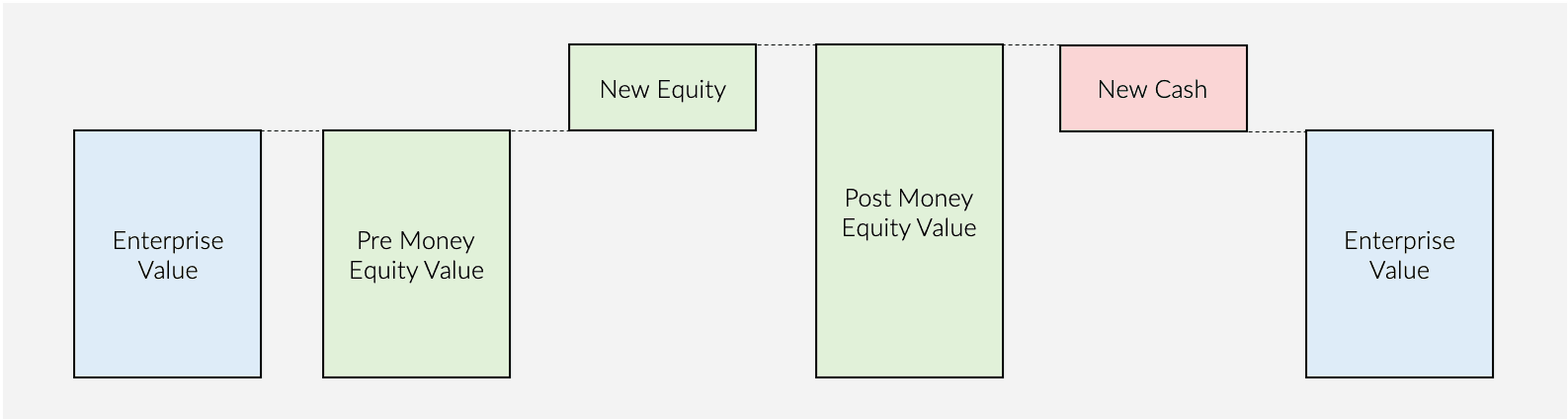

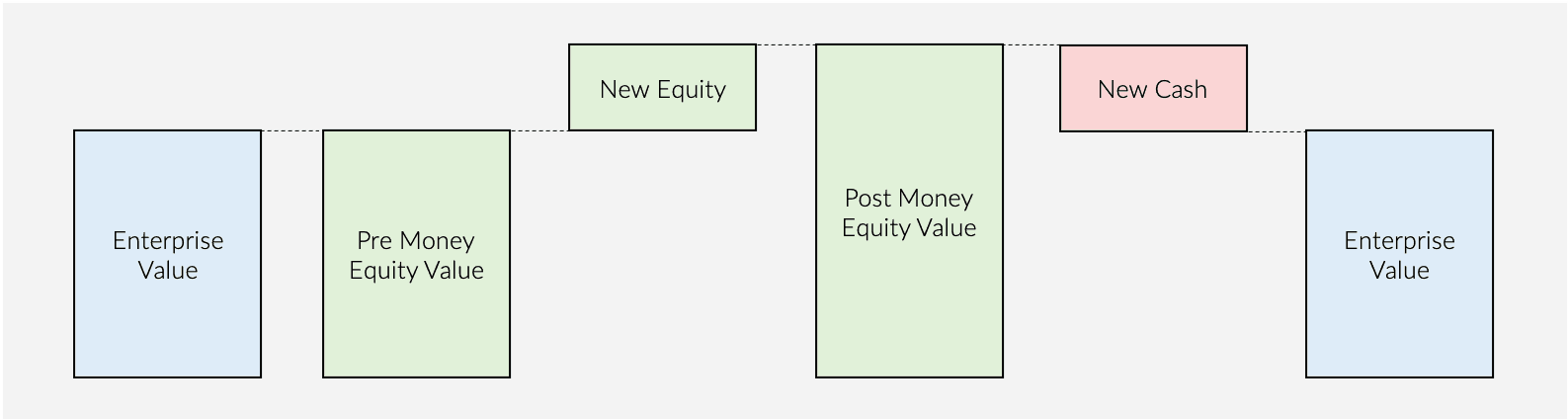

If no one has lent you any money (and debt includes shareholder loans), then your fundraise will look like this:

The newly issued shares represent new equity value, and thus the post-money equity value is higher than the pre-money equity value.

The new cash on the balance sheet is effectively negative net debt and is deducted to reach the post-investment EV – which will always equal the pre-investment EV.

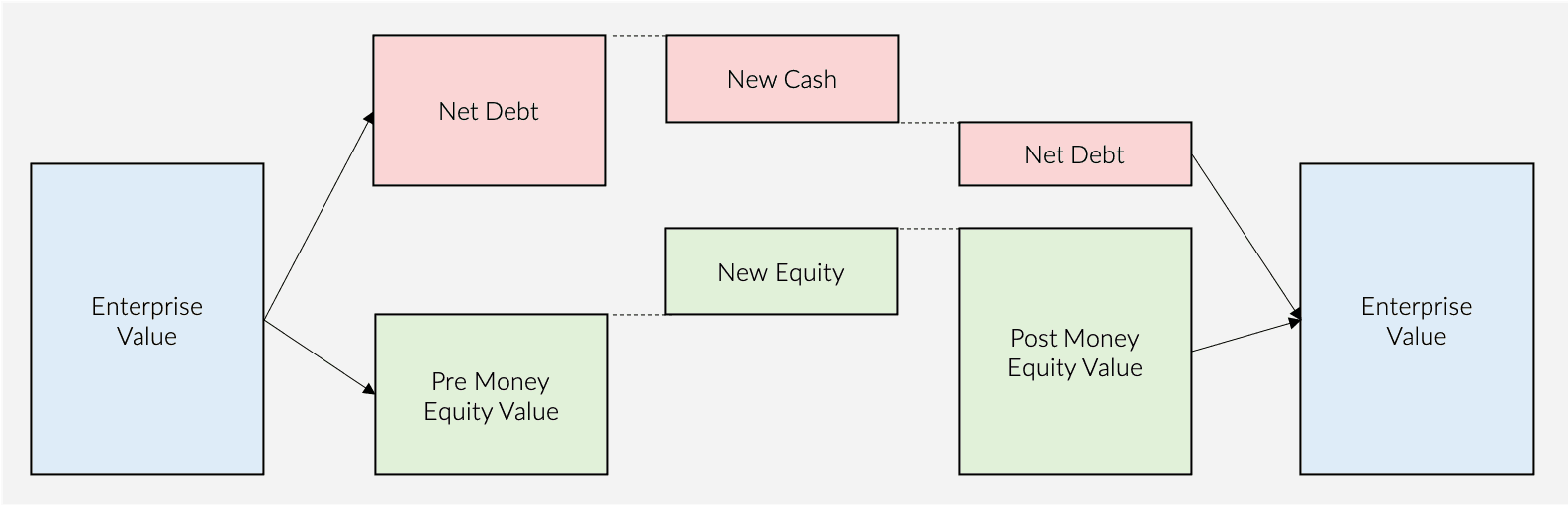

If you have debt or shareholder loans on your balance sheet, then your fundraise will look like this:

The newly issued shares increase the equity value but the new cash reduces net debt and thus EV remains the same.

It is important when pitching to investors to be clear which metric is being used when talking about price or valuation. For seed rounds, it is common to refer to the pre and post-money equity value while making investors aware of any existing debt.

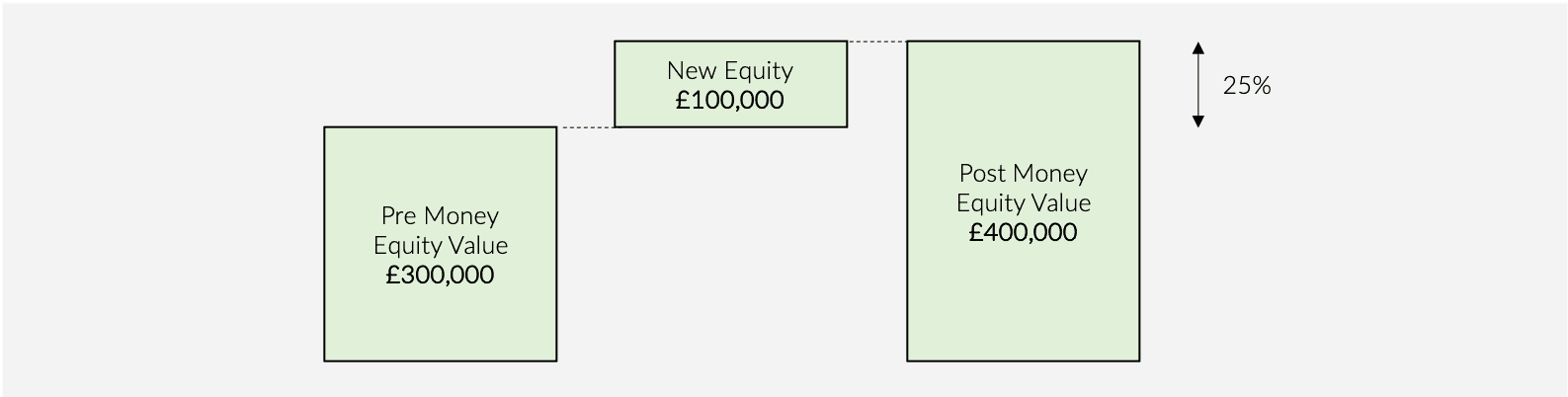

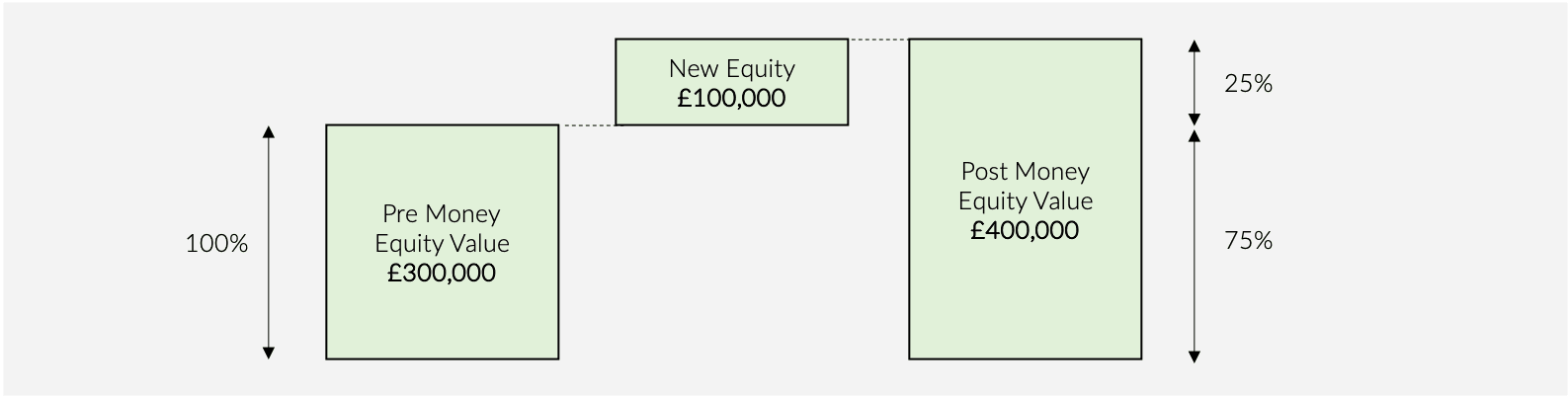

A typical proposal would read as follows:

“We are seeking investment of £100,000 in return for 25% of the equity in the company”

In this example, the implied post-money equity value is:

i.e. £100,000 / 25% = £400,000

The pre-money equity value is:

i.e. £400,000 - £100,000 = £300,000

We focus here on the methods of valuation that are used in practice for early stage companies doing a seed round.

Gather the valuation data of companies that have recently raised funding and that you consider to be similar to your own. Specifically, you want to find out the equity percentage acquired and the amount invested.

This will give you the information you need to calculate the post-money equity value for each transaction, unless it is directly disclosed. If the equity stake is not disclosed, you may be able to find this in their latest annual return on Companies House. There are also databases that are dedicated to collating this data, such as Crunchbase.

For each comparable, do some research into their key KPIs, for example: turnover, rate of growth, profit, number of employees, technology, IP, number of sites / offices / locations. This will give you a sense for how these businesses compare to yours and what may be an appropriate valuation for your business.

For later stage companies, the comparable transactions method is formalised such that multiples of Turnover and EBITDA are established. These multiples are not applied to equity value metrics as they will not be comparable and they must take into account the entire capital structure of the company, i.e. equity value and debt value. The EV of each comparable transaction can be calculated through EV = post-money equity value + net debt. You can find their net debt on their latest filed balance sheet but note that net debt must be the post-transaction net debt and thus deduct the new cash raised. Their Turnover and EBITDA can also be sourced from their latest filings at Companies House.

EV / Turnover and EV / EBITDA multiples can then be produced for each comparable transaction. You can apply the average multiple to your own Turnover or EBITDA to establish an estimate of EV for your business.

Using your forecast financial plan, you can estimate the potential exit value for your company and calculate the expected return to investors.

Most investors assess their returns on a money multiple basis, that is:

Expectations vary significantly according to the sector and individual investment preferences, but are underpinned by the logic that investors will seek a return that is commensurate with the level of risk they are taking on. A very high risk strategy that requires significant investment and entails rapid growth may require a return of 10-20x. A low risk strategy that requires modest investment and growth may require a return of 3-4x. Returns are typically measured over a 3-5 year period.

The first step is to estimate the exit value: how much might someone pay to acquire your business in 3-5 years’ time? If your business is expected to become profitable, you can apply a multiple to your forecast profit in 3-5 years’ time to calculate the Enterprise Value (the price that an acquirer would pay for the business). As discussed above, multiples for comparable transactions can be sourced to provide a justifiable estimate for the multiple applied to your business.

To calculate the return to the investor, first calculate the Exit Equity Value using your forecast net debt:

Their proceeds on exit are calculated as:

Note that this assumes that no further funding was required to deliver the 3-5 year plan – if you do intend to raise further funding, it would be prudent to assume that the investor’s equity stake is diluted by some degree, say, 50%.

If this number is too low, for example, 3.5x when you consider your plan is high-growth and high-risk, then by adjusting the Investor Equity % upwards, you can increase this to what you feel is appropriate.

Now you have the amount that they will invest and the equity stake they will hold, and so:

The pre-money equity value is:

Now that you have an estimate of how much you want to raise and the equity stake you will offer in return, you can calculate the share price. Note that the share price of the company will be the same before the transaction and after the transaction – it follows the same logic as the Enterprise Value – each share does not become worth more purely through raising investment.

And as a final error-check, the share price should also be:

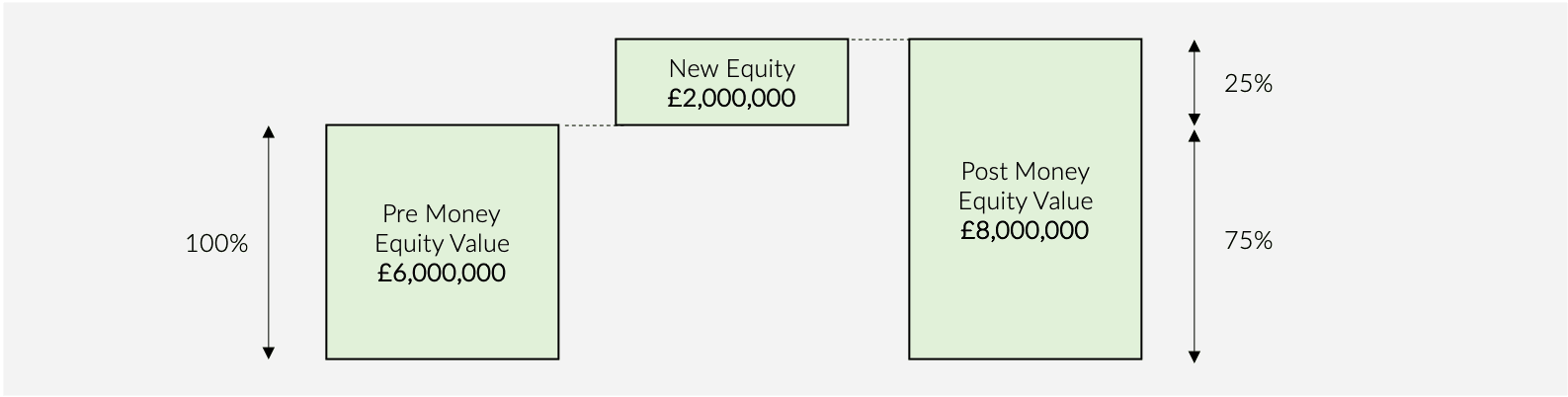

If you are the sole shareholder, this is simple, as following the round you will hold whatever is left of the equity – if new shares representing 25% were issued, then your existing shares will now represent 75% of the equity.

If you have multiple shareholders, it is best to model this through a cap table, but you can also calculate this individually as follows:

Setting out the pre and post shareholder structure

This should be done through a cap table – see our guide on creating a cap table for a seed round.

It is not essential to make a proposal to venture capital firms with regards to the price of the round – most investors run their own valuation and returns models in considering their offers; however, it is important to understand how valuation works so that you can have a meaningful discussion with potential investors, and ultimately judge and respond to offers.

If you are raising from a group of investors, then you would typically negotiate and agree the valuation with the lead investor in the first instance, which may then be tweaked depending on how discussions go with the other investors. If you have no lead investor, you may find it is simply more practical to provide a proposal on valuation than to rely on individual proposals from investors. Certain corporate-backed and strategic investment funds also rely more heavily on businesses conducting their own valuation analyses, compared to traditional venture capital funds.

It is very difficult to price small, high growth companies, as it involves a significant amount of judgement and guesswork. The core valuation principles that apply to large, listed companies, stock markets and even private equity backed companies, are difficult to apply as they rely heavily on multiples of profit and do not take into account the rapid growth rate of many small companies.

Ultimately, the theorems underpinning corporate valuation are a representation of the collective view held by investors of an appropriate risk-adjusted return. Therefore, once you have a starting point for discussion with investors, you will soon find out whether they agree that it represents an attractive risk-adjusted return through uptake and / or negotiation. The objective being to settle on a price that all parties are comfortable with and represents a fair return for both existing shareholders and new investors.

The value of a business is called the “Enterprise Value” or “EV”. It is a common misconception that valuation increases when you raise equity – this is incorrect. It is not possible to alter the value of a company through changing the way in which it is financed – only through utilising that investment to generate more money, can value be created.

As a side note - it’s worth being aware that this misconception, surprisingly, has also made its way into the venture capital funds themselves. If investors refer to the value increasing upon investment, they are referring to the equity value alone, and not the value of the business.

The EV (the value) of a business remains the same before and after raising money. The terms pre-money equity value and post-money equity value refer to a portion of the EV only.

The EV represents the total value of claims that each stakeholder has on the business. Stakeholders comprise:

Debtholders rank in priority to shareholders.

EV is essentially the value owned by the debtholders (“Debt Value”) plus the value owned by the shareholders (“Equity Value”), minus the cash sitting on the balance sheet. If there is cash on the balance sheet, then this can theoretically be used to pay back some of the debtholders. Debt minus cash is referred to as Net Debt and therefore:

If the business has no debt and no cash (and debt includes shareholder loans), then the fundraise will look like this:

The newly issued shares represent new equity value, and thus the post-money equity value is higher than the pre-money equity value.

The new cash on the balance sheet is effectively negative net debt and is deducted to reach the post-investment EV – which will always equal the pre-investment EV.

If you have debt or shareholder loans on your balance sheet, that exceed your cash balance, then your fundraise will look like this:

The newly issued shares increase the equity value but the new cash reduces net debt and thus EV remains the same.

It is important when pitching to investors to be clear which metric is being used when talking about price or valuation. For venture rounds, it is common to refer to the pre and post-money equity value while making investors aware of any existing debt and cash balances.

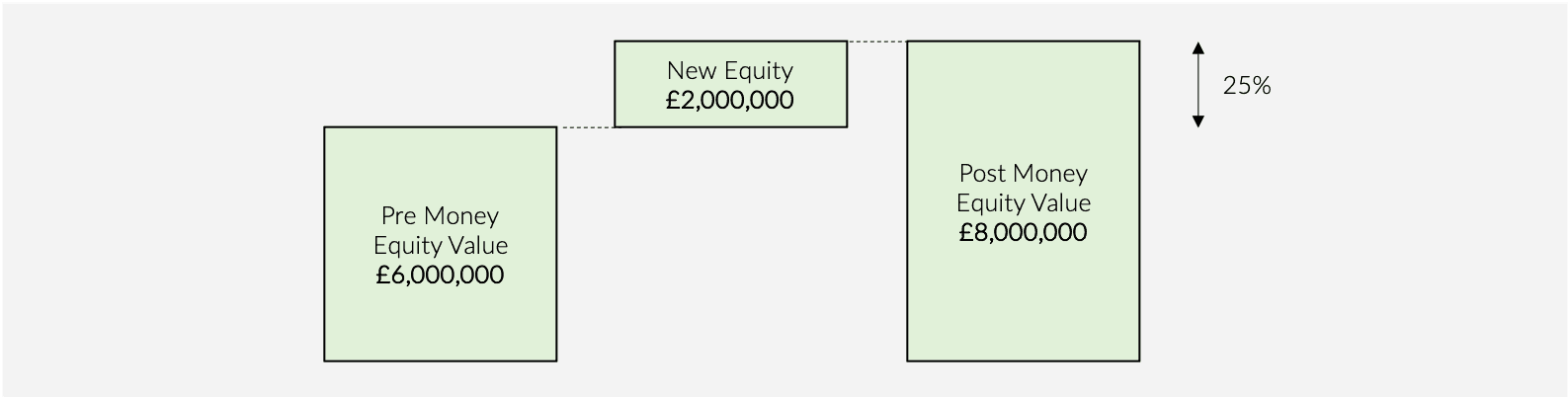

A typical proposal would read as follows:

“We are seeking investment of £2,000,000 in return for 25% of the equity in the company”

In this example, the implied post-money equity value is:

i.e. £2,000,000 / 25% = £8,000,000

The pre-money equity value is:

i.e. £8,000,000 - £2,000,000 = £6,000,000

In the same way that investments work in other industries, such as in the commodities, corporate bonds and property markets, the fundamental principle of corporate valuation is that the price paid should be such that, when the investor exits their investment, they receive an appropriate return on their money for the risk that they have taken on.

In order to grow and raise further funds themselves, venture capital funds wish to demonstrate to their own investors that not only will they generate an appropriate return for the risk, but they will generate above-average returns (something investment bankers call “alpha”).

Valuation is therefore important – if too high a price is paid across too many investments, the fund will not generate a sufficient return.

Venture capital funds typically measure the risk adjusted return in two ways:

The former is the most commonly used when assessing the valuation of potential investee companies, so to keep this simple, we will focus here.

To generate an appropriate risk adjusted return across the fund, venture capital firms must take into account the failure rate of small companies. When assessing new investment opportunities, it is not uncommon for funds to target potential returns of 10-20x their initial investment.

A 10x return on a £2m investment requires £20m to be returned to the fund on exit – if that occurs over a 5 year period, it represents an IRR of almost 60%. This is why venture capital is a more expensive form of financing when compared to bank loans or mezzanine financing, but it is also significantly riskier for the fund, as it is highly likely some or many of their investments will underperform or even fail.

It is the strategy of almost all venture capital funds, to generate this return through increasing the value of the business, not through attempting to under-pay for a company. A fair valuation on entry and exit distils the investment thesis down to the drivers of equity value over the investment horizon. So how do you estimate fair value on entry? One such method is known as the multiple method.

The multiple method relies on the assumption that companies operating within similar industries and with similar characteristics, are worth the same, or a similar, multiple of turnover and / or earnings.

The greater the likelihood of higher future earnings and therefore higher future returns, and the more certain those earnings are, the higher the multiple will be. For example, businesses and industries that are growing very quickly will typically command higher multiples of their current earnings. Businesses with good revenue visibility, for example those with long term customer contracts or recurring revenue, will also attract higher multiples because future earnings are more certain.

For example, a technology business with recurring revenues, good visibility of forecast income that is growing rapidly may be valued at 2.0x turnover and 12.0x EBITDA (Earnings before Interest, Tax, Depreciation and Amortisation). A similar business that is growing more quickly could be valued at 2.5x turnover and 15.0x EBITDA.

To gather applicable multiples to apply to your company’s turnover and EBITDA (if profitable), you can look at listed companies and comparable transactions. Here we will focus on comparable transactions as these are most relevant to venture rounds. The aim here is to find out what other investors and buyers have paid for businesses that are similar to your own.

The first step is market research – who has invested in your industry and who has been acquired? There are a few good sources of this information, including Crunchbase. You could also check the websites of private equity or venture capital funds to see if they have acquired or invested in anything in your industry, and search the web for press releases relating to the deals. Try to find relatively recent investments (in the last 5 years).

For each acquisition, wherever the data is available (as it often is not), note down:

For each fundraise, note down:

For the company’s financials, you may need to do a search of Companies House to review the accounts filed at the time.

Next calculate approximate Turnover and EBITDA multiples for each transaction. For acquisitions, this will be:

For investments, first estimate the post money equity value:

Then calculate the pre money equity value. In a business with minimal or no debt and cash, this is a close proxy for the Enterprise Value:

To be theoretically accurate, you should calculate the EV using the net debt of each company; however, this is arguably an onerously detailed approach as you are looking for a guide, not an exact metric. If using the pre money equity value as a proxy for EV then:

You will now have a set of Turnover and EBITDA multiples (though most likely fewer of the latter if some are loss-making companies). Take the average or a weighted average, if certain companies are more similar to yours than others, and apply these multiples to your own Turnover and EBITDA:

If your business is loss making, then only the Turnover approach will apply. If your business is profitable, and generating what you consider to be a steady-state margin, then the EBITDA approach should take precedence over Turnover, as investors place greater importance on the generation of profit than turnover.

With an estimate of your company’s EV, you can calculate the pre-money equity value:

Then the equity stake you would offer to investors is:

Using your forecast financial plan, you can estimate the potential exit value for your company and calculate the expected return to investors, ensuring this is likely to be sufficiently high for them to be interested.

Returns are typically measured on a 3-5 year investment horizon. In this example we will assumed 5 years:

Apply the average multiple used above to your Turnover and / or EBITDA in year 5 to calculate an estimate of the exit EV (i.e. the price that someone might pay for the business at that time). Note that you can use a different multiple on entry and exit as the metrics of the business may have changed. A lower growth rate would imply a lower multiple, but if the business is larger and more established, this could be justifiably left as is. Value that is not reflected in income or earnings could justify a higher multiple, for example, brand value or IP.

Calculate the proceeds to all shareholders:

Then investor proceeds on exit are calculated as:

Finally, calculate the investor’s expected return:

If the return looks too low relative to the riskiness of the business plan, then you can adjust the following:

At the end of this exercise, you should have a broad estimate of the equity stake to offer to, or accept from, investors in return for their investment, and relevant market data to back this up.

Note that the share price of the company will be the same before the transaction and after the transaction – it follows the same logic as the Enterprise Value – each share does not become worth more purely through raising investment.

And as a final error-check, the share price should also be:

If you are the sole shareholder, this is simple, as following the round you will hold whatever is left of the equity – if new shares representing 25% were issued, then your existing shares will now represent 75% of the equity.

If you have multiple shareholders, it is best to model this through a cap table, but you can also calculate this individually as follows:

Setting out the pre and post shareholder structure

This should be done through a cap table. If you don’t have a cap table set up, you can use our dedicated venture-stage cap table resource [LINK].

Early stage investments often rely disproportionately on future customer acquisition relative to historic trading. For this reason, it is a good idea to prepare a customer pipeline analysis before putting together the more detailed financial model. It is also something you may choose to summarise in the investor presentation.

A customer pipeline analysis is a table that sets out the current and new customer assumptions that underpin the company’s forecasted turnover. It does not have to align exactly with forecast turnover, but can be used to illustrate to investors how achievable the forecasts are and to what extent they are underpinned by secured customers and ongoing discussions.

While each business will have a different pipeline, the common objective is to demonstrate realistic and backable assumptions and strong traction.

This is most relevant to B2B businesses. If you are a B2C business with a significant number of users / customers, we recommend including user growth and price per user assumptions within the forecast financial model.

The extent of variability between businesses means that it is not practical to start from a template – so instead we’ll walk you through how to create one from scratch, to align with your business.

Step 1 – Segment and Describe

In Excel, create a list of all of your current customers and potential customers with whom you are in discussions. In the adjacent column, write a few words describing what the business does or the sector they operate in – investors will be interested to know who your customers are.

Segment customers into categories that represent how progressed they are. We recommend between 2 and 5 stages, for example:

Or:

Sort the list by category so that the most advanced customers are at the top of the list.

Step 2 – Apply Probability Weighting

Allocate a probability of success / conversion to each category, to reflect the reality that not all discussions will result in a sale, for example:

Step 3 – Input Turnover Assumptions

The pipeline should ideally cover a period of two years – the first being the current fiscal year and the second being a forecast year. If you have good visibility beyond that, then you can extend it, but most businesses do not.

Create a column for “Actual or Expected Start Date”

Create a column for each month and input actual Turnover figures for all existing / secured customers up to the present month.

Then, for each customer:

Step 4 – Aggregate

Create a “Total” column at the end of year one and year two, that sums up the monthly Turnover to give total Turnover for that fiscal year by customer.

Create an adjacent column entitled “Proportion of Total Turnover” and calculate the percentage contribution of each customer to the years’ total Turnover. This is an important metric for investors as it illustrates any customer concentration.

A common mistake is to assume that Cash is equal to Turnover.

For example, a subscription business that charges an upfront annual fee of £12,000 in month one, should not input £12,000 as Turnover in month one.

While there are accountancy nuances, the principle that investors follow is that Turnover should be recognised in the month to which the product or services relate.

The subscription business provides access to their product for the entire year, and therefore Turnover is spread evenly over this period. Turnover in month 1 is in fact £1,000, not £12,000.

Getting Turnover right is important to investors as it helps them to assess the growth rate of the business and margin. It is particularly relevant in the definition and calculation of Monthly Recurring Revenue (MRR). If you are unsure of how this applies to your business, one of our consultants would be happy to help – you can view our consultancy services via your dashboard.

Investors in a seed round will not be expecting an all-singing, all-dancing financial model; however, they will expect to see basic figures to help them to understand:

Regardless of what your investors may or may not expect, as a founder it’s useful to have an idea of how the business is expected to grow and how much funding it requires to do so.

Our basic seed round template is quick and easy to complete and tailor. Alternatively, it can be used as a guide as to what investors will expect to see and thus what may need to be added or amended in your existing model.

Input your company name and the current fiscal year end – these inputs will change the column headings throughout the model.

The P&L starts with Turnover and allows for 3 different categories, each with their own Gross Profit so that you can model different margins, if desired. Add or remove categories as necessary to suit your business. You may also wish to add sections above Turnover that include the key components of Turnover, again, tailored to your business; for example, price and volume, number of users and income per user.

Forecast Turnover utilises a year on year growth rate assumption, i.e. how much Turnover grows from January one year to the January of the following year, thus taking into account any seasonality. For an annual growth rate of 30%, input 30% in every month of the relevant year. For most small businesses, growth rate steadily declines, so it may start at 150% in January and fall to 50% in December of a particular year.

The model provides for five categories of overhead costs. Add or remove rows here as appropriate and label according to your business.

Input the relevant tax rate – this may be zero if the company is loss making.

There is nothing to add here as it is automatically generated from other inputs, unless you want to model additional balance sheet items.

To keep the model simple and easy to apply to different businesses, it excludes: intangible assets such as goodwill, prepaid expenses, accrued revenue, deferred revenue or accrued expenses. If you wish to model these, add these as extra lines in the Balance Sheet and Cash Flow.

Note that the Balance Sheet won’t balance until all of the inputs throughout the model have been populated. Once this has been done, if there is a consistent error in the balance, for example, 100 every month, then the starting shareholders equity balance must be amended by that amount in the Balance Sheet Schedules tab.

The cash flow statement is generated automatically from other inputs so there is nothing to add on this tab, with the exception of the closing cash balance at the start of the period. The data for the cash flow graph is included in this tab.

The model allows for up to two lines of debt, which could be overdrafts, term loans and/or shareholder loans. If you have more than two, copy and paste one of the schedules and add a line into the Balance Sheet and Cash Flow. Rename each line of debt accordingly, input the applicable interest rates, current balances and any anticipated drawdowns or repayments.

Input the current tangible assets balance and any forecast capital expenditure – these are the expenses that you capitalise as opposed to expense in the P&L, for example, purchase of assets. The model calculates Capital Expenditure as a percentage of Turnover to provide a sense check.

The model assumes a depreciation policy of 20% of capital expenditure per annum, or 1.7% per month – this can be amended as appropriate and is intended to be an approximation, as it is applied to the monthly opening fixed asset balance.

Input the trade debtor balance for each month of the current year, i.e. the balance at the end of each month representing income that has been invoiced but not yet received in cash. The model uses the current year data to calculate average debtor days, i.e. the number of days it takes for customers to pay, which may inform the assumption that you use for debtor days in the forecast years.

Complete the inventory / stock and trade creditor schedules in the same way.

Input the starting shareholders equity balance and any anticipated equity investment or dividends.

Here are a few house-keeping checks:

A balancing balance sheet

Make sure your balance sheet balances, i.e. that total assets equal total liabilities plus shareholders equity. If it doesn’t balance, the model will show you what the delta is each month. If this delta is consistent every month, there is likely an error in the starting shareholders equity balance. If the delta increases each month, then it is likely that one of the items included in the balance sheet does not have a corresponding entry in the cash flow or vice versa (which may occur if you have added extra line items).

Cash headroom

A review of the cash graph will give you a sense for whether the model approximates your anticipated cash flow and for how much funding you need to raise.

Turnover and margin trends

Check that the trends in turnover and margins look sensible, realistic and there are no unusual movements. There is an annual summary to the right of each statement to provide the macro view. Ensure that the figures fairly reflect what you intend to achieve as a business and can be relied upon by investors.

A financial model is an essential tool in undertaking a fundraise – it helps a business to understand how much capital to raise and when to do the raise. It portrays the business plan to prospective investors, enabling them to sense check forecast performance against recent historic trading, assess the riskiness of the investment thesis, calculate the cash burn rate, assess and sensitise key driving assumptions and model their expected returns.

We have built a simple Excel template that covers the basic figures that investors expect to see across all business types. This resource provides step by step instructions on completing the template for your business below (as well as prompts inside the model). Alternatively it can be used as a guide to amend and improve your existing model.

We recommend adding a tab that displays the key KPIs for the business – this cannot be templated as it varies for each and every business. These KPIs may also be linked to the turnover and cost assumptions in the model, if applicable.

These KPIs may include standard financial metrics, such as Turnover Growth and Gross Margin (included within the model), and key drivers of growth and return, such as number of users, price per user, volume, number of sites / locations, cost of customer acquisition, customer payback, return on investment etc.

The model includes two years of historic P&L data from Turnover to EBITDA. It does not require historic balance sheet and cash flow data as this is rarely held by early stage companies and is not always required by investors (although the cells have been left populated with “n/a” in case you want to include this). Instead, the closing balance sheet for the most recent fiscal year end is used as a starting point for the cash flow forecast. Historic P&L data is of particular interest to investors for the purposes of assessing the pace of growth to date and sense checking the forecasts. The balance sheet and cash flow data are of greater relevance to the future funding needs of the business. Investors may wish to diligence the historic cash flow of the business later in the process – at this time, the historic cash flow data can be added to this model, or a standalone model may be built to specifically address their question.

The first step is to complete and tailor the template for your business, or use this as a guide to review and amend your own financial model.

Input the company name and the current fiscal year end – these inputs will change the column headings throughout the model.

Input historic P&L turnover and costs for the past two years (if applicable) to demonstrate recent trading history.

The P&L allows for 3 different categories of Turnover, each with their own Gross Profit so that you can model different margins, if desired. Add or remove categories as necessary to suit your business.

Forecast Turnover utilises a year on year growth rate assumption, i.e. how much Turnover grows from January one year to the January of the following year, thus taking into account any seasonality. For an annual growth rate of 30%, input 30% in every month of the relevant year.

Forecast Cost of Sales are based on a percentage of turnover.

The model provides for five categories of overhead costs. Add or remove rows here as appropriate and label accordingly. If you would like to include more detail, we recommend adding an additional “Overheads” tab that includes assumptions such as growth rates, to calculate forecast costs. It may also be helpful to provide a breakdown of salaries by employee.

Input the relevant tax rate – this may be zero if the company is loss making.

The key line items here are driven by separate schedules on the “Balance Sheet Schedules” tab and therefore do not require editing.

Lines are also included for Prepayments, Other Debtors, Accrued Revenue, Deferred Revenue, Other Creditors and Accrued Expenses. These line items may not be applicable to the business and will depend on your working capital cycle and the nature of certain payments, such as rent. To keep the model simple, these can be removed or left blank. If removed, make sure to remove the corresponding line items on the “Cash Flow” tab.

Below the balance sheet is a “Difference in Balance” row that should show “0” in every month, i.e. Total Assets should always equal Total Liabilities and Equity such that the balance sheet balances. Note that this row may show a delta until all inputs throughout the model have been populated. Once this has been done, if there is a consistent error in the balance, for example, 100 every month, then the starting shareholders equity balance must be amended by that amount in the Balance Sheet Schedules tab.

The cash flow statement is generated automatically from other inputs so there is nothing to add on this tab, with the exception of the closing cash balance for the most recent fiscal year. The data for the cash flow graph is included in this tab.

The model allows for up to four lines of debt, which could be overdrafts, term loans, shareholder loans or venture debt. Rename each line of debt accordingly, input the applicable interest rates, current balances and any anticipated drawdowns or repayments.

If you have more than four lines of debt, copy and paste one of the schedules and add the corresponding lines to the Balance Sheet and Cash Flow.

Input the current tangible assets balance and any forecast capital expenditure – these are the expenses that you capitalise as opposed to expense in the P&L, for example, purchase of assets. The model calculates Capital Expenditure as a percentage of Turnover to provide a sense check.

The model assumes a depreciation policy of 20% of capital expenditure per annum, or 1.7% per month – this can be amended as appropriate. This rate is applied to the monthly opening fixed asset balance and thus is an approximation and assumes ongoing capital investment. To model this accurately, create an additional tab called “Fixed Asset Register” and create a schedule for each individual asset. The depreciation row should take the opening balance of the asset so that the value decreases to zero by year 5 (assuming a 20% annual rate of depreciation). Note that this level of detail is not likely to be required by investors because depreciation does not impact cash flow, EBITDA or equity returns.

A goodwill schedule is included for businesses that have undertaken acquisitions in the past. If this is not the case the schedule can be left blank or deleted (if deleted, remember to remove the corresponding amortisation and acquisition lines in the P&L, Balance Sheet and Cash Flow).

Input the trade debtor balance for each month of the current year, i.e. the balance at the end of each month representing income that has been invoiced but not yet received in cash. The model uses the current year data to calculate average debtor days, i.e. the number of days it takes for customers to pay, which may inform the assumption that you use for debtor days in the forecast years.

Complete the inventory / stock and trade creditor schedules in the same way.

Input the closing shareholders equity balance for the most recent fiscal year end, and any forecast equity investment or dividends. It is common to exclude the current fundraise from the model until negotiations with investors are more advanced and the specific commercial terms can be modelled.

Here are a few house-keeping checks:

A balancing balance sheet

If the balance sheet doesn’t balance, the model will show you what the delta is each month. If this delta is consistent every month, there is likely an error in the starting shareholders equity balance. If the delta increases each month, then it is likely that one of the items included in the balance sheet does not have a corresponding entry in the cash flow or vice versa (which may occur if you have added extra line items).

Cash headroom

A review of the cash graph will give you a sense for whether the model approximates your anticipated cash flow and an idea of how much funding you require.

Turnover and margin trends

Check that the trends in turnover and margins look sensible, realistic and there are no unusual movements. There is an annual summary to the right of each statement to provide the macro view. Ensure that the figures fairly reflect what you intend to achieve as a business and can be relied upon by investors.